Reasons for the polyethylene price increase in February 2024

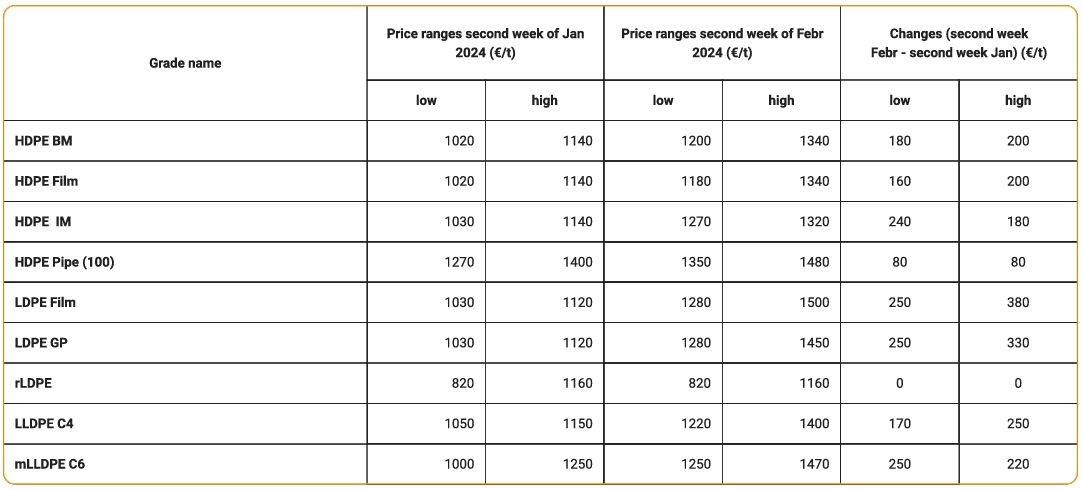

Between January 2024 and February 2024, there will be a dramatic increase in polyethylene prices of EUR 200-380/t compared to the levels at the beginning of January 2024. The analytical company myCeppi consulting has provided information on the situation in the commodity plastics market.

The price changes for full truckloads are shown in the table below, which covers the period from the second week of January to the second week of February.

| |

The reason for the price increases can clearly be traced back to the extremely limited supply. Behind the limited supply are, on the one hand, the planned and unplanned shutdowns of Central European polyethylene producers.

Ongoing maintenance / outages / malfunctions:

MOL Group - Slovnaft LDPE-4unplanned shutdown at the plant (220 kt/year LDPE capacity), the shutdown is expected to last 7-9 weeks. Due to the shutdown, the capacity of both the Bratislava Steam-cracker and the PP plant was reduced.

Rompetrol LDPEis still standing due to monomer supply problems at the plant (LDPE capacity of 60 kt/year), a restart is only expected if market prices ensure profitable operation from purchased ethylene. MOL Group LDPE- production problems at the plant of MOL Petochemicals in Tiszaújváros (65 kt/year capacity), production is expected to be restored already in February.

Expected maintenance / outages:

Orlen-Unipetrol HDPE planned shutdown in Litvínov from April 8, 2024 (270 kt/year capacity), the expected duration of maintenance is 30 days. Planned shutdown at in May, in Plock, (100 kt/year capacity) planned duration is 3 weeks.

HIP-Petrohemija LDPE HDPE planned maintenance in Pancevo between March 11 and April 25, 2024 (60 kt/year and 90 kt/year capacity affected)

In the case of the LDPE grades showing the largest price increase, all Central European production capacities are affected, the LDPE plants have either shut down or are preparing for maintenance. But a part of the HDPE plants, roughly 40% of the Central European capacities, are affected or will be affected by production restrictions.

Due to the deterioration of the security situation in the Red Sea, import shipments from the Middle and Far East are significantly delayed by 4-6 weeks. In addition, sea freight costs and container rental fees have increased significantly. This means a price increase of €100-200 per ton of imported polymer. In addition, the North American polyethylene producers not affected by the Red Sea crisis also implemented a significant price increase of $0.05/lb, i.e. more than €100. This especially affects LLDPE, HDPE and LDPE grades.

Western European polyethylene producers are also struggling with production problems. In fact, in the second week of February, all Western European manufacturers reported an “order stop”.

We expect the supply to expand gradually from the end of February. The arrival of the delayed import shipments is expected from that time. However, the supply will reach the usual level only in the second half of May, when the maintenance will be completed and the polymer stocks of the Central European polyethylene producers will be replenished.

- autor:

- L�szl� B�dy

-

myCEPPI

myCEPPI provides a weekly price report for commodity plastics.

- www.myceppi.com

- J�zsef krt. 69, Budapest

You might also be interested

-

ECT, s.r.o.: Your reliable partner for quality regranulates and prime/NTP materials

ECT, s.r.o. is a renowned supplier of plastic regranulates and Prime/NTP materials with a long tradition and commitment to providing the highest quality products. Our offer includes a wide range of materials that meet even the highest requirements of our...

-

K.D. Feddersen Distribution expands its TRINSEO portfolio with ALTUGLAS� brand

Hamburg-based plastics distributor K.D. Feddersen GmbH & Co. KG and its European subsidiaries have been selling TRINSEO thermoplastic elastomers since 2021. With the ALTUGLAS� brand, PMMA is now also coming to the European...

-

MOL's �1.3 billion polyol complex in Tisza�jv�ros inaugurated

- 15.05.2024

- Suppliers of raw materials

- Elastomers

The �1.3 billion project is MOL's largest organic investment to date, for which it has also received support from the Hungarian state. The complex will produce raw materials for durable plastic consumer goods such as bed mattresses, moulded car seats, insulation for houses and elastic rubber soles...

-

MOL Group wants to achieve carbon neutrality with its smart transformation

MOL Group has updated its long-term strategy SHAPE TOMORROW. The goal is a greener, more self-sufficient and competitive...

-

VACULA s.r.o. is introducing proven cleaning granules RAMCLEAN from POLYRAM to the market

VACULA s.r.o. presents proven cleaning granules RAMCLEAN from POLYRAM. These are cleaning agents for plastic production with patented composition. They are safe, effective and compatible with both extrusion and injection moulding of...

-

ORLEN has launched mobile app with loyalty programme

The ORLEN filling station network has launched a mobile app that offers customers benefits such as a loyalty programme and navigation to the selected petrol station. Customers can use the ORLEN app to earn points for payments when purchasing fuel, goods and services at full and self-service petrol...

-

Innovation for a sustainable future: SILON CZ R&D takes research and development to the next level

- 08.03.2024

- Suppliers of raw materials

- Technical plastics

On the 1st January 2024, SILON Group welcomed a new addition � SILON CZ R&D. The decision to found an independent subsidiary focused on research and development is due to the high level of interest in expert support for R&D projects on the part of both customers and government organisations on a...

-

ORLEN expands its fuel station network in Europe

Following the acquisitions in Austria, Germany, Slovakia and Hungary, ORLEN's station count has surged by almost a third over the past year. The Group is currently finalising the purchase of more than 60 service stations in...

-

Safic-Alcan strengthens its position in Central Europe by establishing a Slovak branch

- 14.02.2024

- Suppliers of raw materials

- Additives for plastics

- Compounds

- Technical plastics

- TPU - thermoplastic elastomers

Safic-Alcan, a leading global distributor of specialty chemicals, is thrilled to announce the expansion of its presence in Central Europe through the establishment of a new subsidiary office in...

-

K.D. Feddersen Distribution expands its portfolio with Celanese's Crastin�

- 31.01.2024

- Suppliers of raw materials

- Technical plastics

As of January 2024, K.D. Feddersen Distribution in Europe is expanding its extensive PBT range from Celanese to include new material grades for food applications, halogen-free flame retardants and high creep resistance...

Branch Dictionary